Secure Your Future with Guaranteed Lifetime Income

Balanced Allocation Lifetime Income Rider® Flex GrowthSM

A Flexible Opportunity to Grow Retirement Income

The optional Flex Growth – Balanced Allocation Lifetime Income Rider® (BALIR®) option offers a source of retirement income you canʻt outlive.1 BCA 12 2.0 fixed indexed annuity offers potential growth for your retirement savings with protection from downside market risk. Available for an additional charge, Flex Growth provides three powerful ways to grow future lifetime income:

- A 20% Income Base Bonus immediately increases the Income Base, which is used to determine future lifetime income.2

- Guaranteed 4.5% Annual Increases to Your Income Base credited daily throughout each policy year.

- 200% of Any Interest Earnings, if greater than the Guaranteed 4.5% Annual Increase, will be credited to your Income Base at the end of every 2-year term.3

For more information on the Income Base and Income Base Bonus, please contact your insurance professional to see the Additional Information insert.

Planning for Guaranteed Lifetime Income

Objective: Sarah needs to create a source of income that will last throughout retirement, and she wants guaranteed growth with the opportunity to participate in upside market potential.

Solution: Sarah allocates $100,000 of her retirement savings to BCA 12 2.0 with the Flex Growth option. A 20% Income Base Bonus immediately increases her Income Base, which will be used to determine future guaranteed lifetime income.

Result: Over the next 16 years, Sarah’s Income Base grows by the greater of a guaranteed 4.5% compound annual increase or 200% of Interest Earnings, credited to her Income Base every two years. By age 82, Sarah’s Income Base has increased to $1,622,791.

This is a hypothetical example to show how BCA 12 2.0 and Flex Growth can work. Your experience will differ. Past performance is no guarantee of future performance.

Harnessing Market Growth and Guarantees

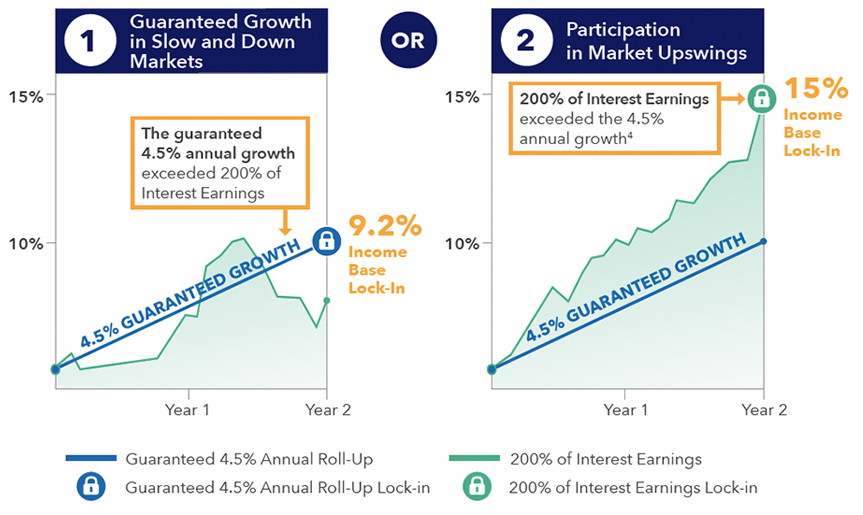

Flex Growth helps you harness market growth and guarantees by automatically providing the greater of a guaranteed 4.5% annual roll-up and a percentage of any Interest Earnings, credited to your Income Base every two years.

Receive the Higher of Two Values

These graphs track the hypothetical progression of 200% of Interest Earnings over a 2-year term. This calculation uses the base contract Balanced Allocation Value (BAV), which is calculated daily but is not available for surrender. For additional information on the BAV, please contact your insurance professional to see the Additional Information insert (83151).

This is a hypothetical example to show how BCA 12 2.0 with Flex Growth can work. Your experience will differ. Past performance is no guarantee of future performance.

The graph above is for informational purposes only and intended to demonstrate how the Income Base can grow. It is hypothetical and does not demonstrate actual performance of any BCA 12 2.0 or Flex Growth contract or index. This does not demonstrate the potential impact of Annual Strategy Charges and withdrawals, which will reduce the Income Base. Please remember that the Income Base is used for calculating Lifetime Income Withdrawals and cannot be withdrawn in a lump sum. The length of each term is two years. For more information about Flex Growth, please ask your insurance professional for an illustration.

Hypothetical Assumptions: $100,000 premium in BCA 12 2.0 with Flex Growth, 390% Participation Rate, 0.95% Annual Strategy Charge, 1.00% Annual Income Rider Charge Rate and no other optional riders elected. Based on index performance for the most recent 10 calendar years, repeated every 10 years, for the Citi Grandmaster Index.

{kind=link}

Every two years, the greater of a guaranteed 4.5% annual roll-up or 200% of any Interest Earnings is credited to Sarah’s Income Base, establishing a new locked-in Income Base on which future growth is calculated.

Hypothetical Assumptions: $100,000 premium with BCA 12 2.0 with Flex Growth, 16 years of deferral prior to beginning Lifetime Income Withdrawals, at the following rates: 20% Income Base Bonus, guaranteed 4.5% annual roll-up in years 1-16, Single Life, Level Income Option, 1.00% Rider Charge. Based on the index performance for the most recent 10 calendar years, repeating every 10 years, for the Citi Grandmaster Index. Assumes no withdrawals before beginning lifetime income. The Income Base is used for calculating Lifetime Income Withdrawals and cannot be withdrawn in a lump sum. All values are net of applicable Annual Strategy Charges. For more information, please see the BALIR rate sheet and ask your insurance professional.

Flex Growth is available with select BCA 2.0 FIAs. Rates and product availability will vary by state and results may be higher or lower. See your insurance professional for detailed information.

Key Terms and Definitions

What is a Fixed Indexed Annuity? – A fixed indexed annuity is a contract issued by an insurance company. In exchange for your premium, the insurance company provides the opportunity for growth based in part on the performance of an underlying index, or group of indices, within a larger strategy while protecting your money from downside market risk. All guarantees are backed by the claims-paying ability of the issuing carrier and may be subject to annual charges. Fixed indexed annuities are not stock market investments and do not directly participate in any stock or equity investments or index. It is not possible to invest directly in an index. Other restrictions and limitations may apply. For more information, please contact your insurance professional to see the BCA 12 2.0 product brochure.

Balanced Allocation Lifetime Income Rider (BALIR) – Flex Growth – The BALIR – Flex Growth is an optional rider that must be elected at contract issue and is available for an annual Income Rider Charge of 1.00%. The Annual Rider Charge is calculated at the beginning of every contract year. The charge is deducted in monthly installments from the Accumulation Value and, in some states, the Minimum Guaranteed Contract Value. On the 10th contract anniversary, you may elect to extend Income Base growth up to the 18th contract anniversary. The rider charge may increase by up to 0.20% per year times the number of years extended starting at the beginning of the 11th contract year.

Income Base – The Income Base is used to determine the annual Lifetime Income Withdrawals and Annual Income Rider Charge, if applicable. Flex Growth offers Income Base growth that is the greater of a daily rate that is equivalent to 4.5% annual compound interest and the net of 200% of BCA 2.0 Interest Earnings, if any, minus the Annual Strategy Charge, if applicable. Interest Earnings, if any, are credited to the Income Base until the earlier of Lifetime Income Withdrawals beginning on the 10th contract anniversary (or up to the 18th anniversary if the Income Base growth is extended). If you begin Lifetime Income Withdrawals before the end of a two-year term, interest, if any, will be credited pro rata to the Income Base. The Income Base is not an amount that has a cash value or surrender value that can be paid out partially or in a lump sum. Withdrawals, prior to commencing Lifetime Income Withdrawals, will reduce the Income Base by the same percentage that the Accumulation Value is reduced for the withdrawal. However, the dollar amount of this reduction will not be less than the deduction from the Accumulation Value. After Lifetime Income Withdrawals have commenced, withdrawals up to the Lifetime Income Withdrawal amount will reduce the Income Base by the dollar amount of the withdrawal, while withdrawals in excess of the Lifetime Income Withdrawal amount will reduce the Income Base and future Lifetime Income Withdrawals by the same percentage that the Accumulation Value is reduced for the withdrawal. Withdrawals may also be subject to Withdrawal Charges, Premium Bonus Vesting Adjustments or MVAs, if applicable. For more information, please contact your insurance professional to see the Certificate of Disclosure.

Lifetime Income Withdrawals – Lifetime Income Withdrawals are calculated by multiplying the greater of the Income Base or Accumulation Value by the current Lifetime Income Withdrawal Percentage when Lifetime Income Withdrawals begin. The Lifetime Income Withdrawal Percentage depends on the income option elected and is determined by the “Age” Lifetime Income Withdrawals begin. “Age” means your attained age for Single Life or the younger of your attained age or your spouse’s attained age for Joint Life when your spouse is listed as the sole beneficiary or the contract is jointly owned. In general, the longer you wait to take income, the greater the initial Lifetime Income Withdrawal Percentage will be. When you’re ready to begin Lifetime Income Withdrawals, Flex Growth offers the following options:

- The Level Income Option offers the highest initial amount.

- The Inflation-Indexed Income Option increases the lifetime income annually based on increases in the Consumer Price Return Index, if any. Increases are capped at 10% per year and stop when the Maximum Inflation Adjustment Period has elapsed.

- Earnings-Indexed Income Option may increase the lifetime income at the end of every 2-year strategy term based on the rate of interest credited, if any, to the Strategy Options elected.

The Inflation-Indexed Income Option and Earnings-Indexed Income Option offer less initial income than the Level Income Option but may provide more income over your lifetime due to potential increases after beginning Lifetime Income Withdrawals. Lifetime Income Withdrawals will continue even if they ultimately reduce the Accumulation Value to zero. Withdrawals in excess of the Lifetime Income Withdrawal may be subject to a Withdrawal Charge, MVA and Premium Bonus Vesting Adjustment and will reduce future Lifetime Income Withdrawals. Withdrawals in some instances could terminate the rider. For more information, please contact your insurance professional to see the Certificate of Disclosure and ask your insurance professional. Withdrawals and surrender may be subject to federal and state income tax and, except under certain circumstances, will be subject to an IRS penalty if taken prior to age 59½.